6-NDFL: terms of submission, sample of filling

Reporting 6-NDFL - a new document foremployers. It must be submitted to the supervisory bodies from the 1st quarter of 2016. This document is not drawn up for each individual employee, but for the entire enterprise as a whole. Let's consider further how to fill in 6-NDFL.

General information

First of all it is necessary to know where6-NDFL is presented. The document form, issued in accordance with all the rules, is sent to the same supervisory authority to which the tax is transferred. You can submit a document in two ways: in paper or electronic form. The first option is suitable for those employers whose average number of employees is less than 25 people. Form 6-NDFL can be presented in person or sent by mail. In electronic form the document is sent via the official site of the Federal Tax Service.

6-NDFL: terms of granting

The document is presented quarterly. It must be sent no later than the last day of the 1st month of the next quarter. The legislation provides for liability for those who do not submit the 6-NDFL in time. The terms of the grant can be shifted. In particular, this happens if the deadline falls on a holiday or a day off. In this case, for the entities that have issued the 6-NDFL, the terms of the transfer are transferred to the nearest working day. Norms set the following calendar dates:

- 1-st quarter. 2016 - May 3, 2016.

- Half-year - August 1, 2016.

- 9 months - 10/31/2016.

- For the year 2016 - April 1, 2017.

6-NDFL: sample

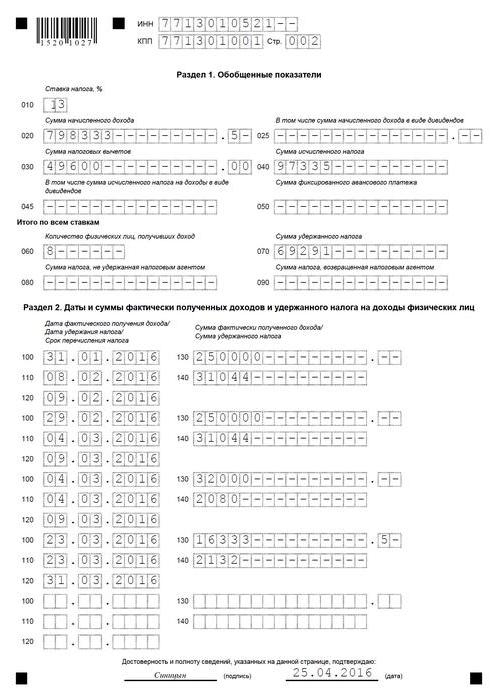

When you make a document, you must comply with a number of general requirements. If we take any correctly compiled example of 6-NDFL, it can be noted that:

- The document is drawn up in accordance with the data present in the accounting registers. In particular, it is a question of accrued and paid income, deductions, calculated and withheld tax.

- Filling of 6-NDFL is carried out with a growing total. First, first quarter, then half a year, then 9 months and a calendar year.

- In the event that all the indicators do not fit on the page, the required number of sheets is drawn up. The final information should be reflected in the last one.

- All pages are numbered (001, 002 and so on) starting from the title page.

- Filling of 6-NDFL should be carried out withouterrors and blots. Not allowed to correct written, including using corrective tools. Also, sheet bonding, two-sided printing is not allowed.

- Since you can fill 6-NDFL by hand or onyou need to know some rules. In particular, the first case uses ink of blue, purple or black. When you design on a computer, the characters are printed at a height of 16-18 points, in the Courier New font.

Rules of registration of fields

In some cases, there may be difficultieswhen entering information in the f. 6-NDFL. A sample document contains fields consisting of a certain number of signatures. In each of them, only 1 indicator should be indicated. The exception is information about the date or value expressed in decimal fractions. The writing of calendar numbers is carried out using three fields. The first two contain 2 familiarity - for the day and month, the last - 4 - for the year. The decimal fraction fits into 2 fields, separated by a dot. Sum indicators and requisites must necessarily be present in the f. 6-NDFL. The form is drawn up separately for each OCTM. The amount of tax is calculated and indicated in rubles. The rounding rules are used. On each page the date of compilation and signature of the responsible person is stamped.

Fields

- "INN" - the figures are indicated in accordance with the certificate of registration with the Federal Tax Service.

- "KPP" - is filled only by legal entities.

- "Adjustment number". This field is set to "000" if the surrender of the 6-NDFL is for the first time, "001" is the first correction, "002" is the second correction, and so on.

- "Period". This field indicates the code that corresponds to the time of delivery.

- "Tax Year" (for example, 2016).

- "Provided to the authority" - this field indicates the code of the FTS to which the document is sent.

- "At the place of registration / location." In this field, the code of the place of providing 6-NDFL is given.

- "Tax agent". In this field, the individual entrepreneur line-by-line inscribes the surname, name, patronymic. Yurlitso indicates the full name in accordance with the constituent documents.

- "OCTMO code". Organizations need to specify it at the location of their location or the location of a separate unit. Entrepreneurs write the code at the address of residence. IP using SPE or UTII, it is necessary to indicate the figures corresponding to the MO in which they are registered in the status of payers.

- "Contact phone" - here, respectively, indicate the number by which the FTS can contact the agent.

- "With the attachment of documents / copies thereof". In this field it is necessary to put the number of pages of papers that confirm this information. If they are not present, dashes are placed.

When is it not necessary to present a document?

Form 6-NDFL is not issued ifduring the period there were no payments to employees and, accordingly, the tax on their income was not withheld. Simply put, it makes no sense to put zeros in the lines. The 6-NDFL declaration is not submitted even when there are no personnel at the enterprise. It is not necessary to make out the document only to the opened (registered) organizations that have not yet started their activities. An entrepreneur or a legal entity may (but not be obliged to) inform the tax service in an arbitrary form about the reasons for which the f. 6-NDFL.

A responsibility

For subjects who need to register6-NDFL, the terms of granting are of great importance. If they are not followed, they will be fined. At the same time, sanctions are imputed to the whole enterprise, as well as to the head. If the delay is not very large, then the amount of the fine is minimal. In this case, account blocking can be used as a measure of influence. Norms provide for 2 types of fines. The first is appointed if the 6-NDFL report was not sent at the due time or presented later. The second penalty threatens the subject if errors are found in the document. Let us consider both cases in more detail.

Late submission of a document

We have already indicated the dates in which we need toprovide f. 6-NDFL. Appointment of a fine for late submission of a document is made within 10 days from the date it was received by the Federal Tax Service. In this case, the inspection may not wait for the completion of the desk audit. If the enterprise is late more than for a month, the fine will be 1000 r. This size is considered to be minimal. For each next overdue month, regardless of whether it is full or not, another 1,000 rubles will be added to the assigned collection. This provision is established in Article 126 of the Tax Code (Clause 1.2). Time of delay will be calculated from the date when the organization presented a report. The head of the company can be fined 300-500 rubles. This sanction is provided for in the Code of Administrative Offenses, in Article 15.6. Tax inspectors have the right to impose this fine without applying to the court.

Account blocking

If the document is not submitted inten-day period with the established dates of the FTS has the right to freeze banking operations with the debtor's financial resources. Such a measure is provided for in Article 76 of the Tax Code (Clause 3.2). Clarifications on the application of account blocking are given in the letter of the Federal Tax Service of August 9, 2016.

Controversial moment

Sometimes in practice there are situations whenthe organization registered at the end of the quarter and has not had time to pay anything to its employees. Accordingly, the 6-NDFL report was not presented to the inspection. Meanwhile, the FTS, not having received the document in time, applies the account blocking to the subject. Many people have a logical question: is this measure legal in this case?

As was said above, Article 76 of the Tax Code in paragraph 3.2 allows the freezing of operations when the ф is not represented. 6-NDFL. Normally, there is no reservation that the lock is used only when there are settlements with the staff. Meanwhile, it was also said above that an enterprise is not obliged to provide f. 6-NDFL, if has no employees or did not pay anything to them in the relevant period. However, the tax authorities themselves repeatedly stated that they expect zero documents from the entities. The fact is that the database does not determine the reason for which no report was submitted. Accordingly, the account is blocked automatically. To defrost, you will have to submit a zero report. During the next day (working), the tax authorities issue a resolution to remove the lock. Such a period is stipulated in paragraph 3.2 of Article 76. Another day will be required to transfer the order to the bank. Usually the exchange of documents is done via the Internet, accordingly, the decision will come to a financial institution quickly enough. Within 24 hours after receiving the resolution, the bank releases the lock. To prevent such problems in the future, experts recommend sending a notice about the lack of settlements with staff and making a decision on this basis about the failure to pay 6-NDFL.

Inaccuracy of information

A fine can be imputed to a subject for any mistakeor inaccuracy in the report. The amount of recovery is 500 rubles. for each page with inaccurate information. This sanction is provided for in Article 126.1 of the Tax Code. In this rule there is no clear list of errors that fall under the category of "unreliable information". In this connection, the relevant decisions are taken directly by the auditors.

Meanwhile, the inspection can not fine everyonesubjects thoughtlessly. As explained by the Ministry of Finance, inspectors should consider each case individually. This means that, before issuing a fine, officials are required to assess the severity of the defect / error. In addition, mitigating circumstances should be taken into account. In particular, a fine may not be imputed if, due to an error, the tax agent:

- Do not understate the amount of mandatory deductions.

- Not violated the interests of physical persons.

- Has not caused damage to the budget.

These points are explained in the letter of the Federal Tax Service of 9.08.2016 As in the case of late delivery of the document, it is allowed to involve not only the enterprise, but also its responsible employees (the head, in particular). Officials may be fined 300-500 rubles.

How to avoid sanctions?

In order not to get a fine, it is necessary to noticeinaccuracies before the tax authorities and correct them. For this purpose, an updated declaration is drawn up. In this case, experts recommend to include in it the correct information on all receipts for the entire period. The updated declaration of 6-NDFL is also presented if in the first document some information is reflected or not fully presented. It is advisable to compile it also in the event that inaccuracy has led to an overestimation of the amount of the deduction. Otherwise, it is possible to impose a fine (500 rubles). The NC requires that only the information that was submitted with errors be included in the updated document. This provision is provided for in Article 81 (paragraph 6). However, the tax inspectorate believes that 6-NDFL can not be filled in this way. In the document it is necessary to show generalized information without breaking them down by payers. If you bring information to one employee, it can distort all information.

Nuances

On the front page when passing the specifiedthe document should be marked with "001 correction number" (if this is the first correction). The rules of registration do not provide for the presentation of an annulment or cancellation calculation. This 6-NDFL differs from the well-known to all references 2-NDFL (it must also be presented). If an error was identified in the same quarter in which it was admitted, it is not necessary to present the specified document. Instead, the inaccurate information is reversed before the end of the reporting period, and the settlement is processed in the usual manner.

Is it necessary to clarify the calculation if the desk audit is completed?

Let us consider the case. The enterprise was mistaken at registration of 6-NDFL for 6 months. In lines 110 and 120 of the second section, the same calendar amounts of withholding and tax deductions were indicated. It would be correct to set the deadline for payment by the next working day after the withholding. At the same time, the deduction was carried out on time. There was a question: whether it is necessary to specify information if the enterprise was not late with the tax, and the office audit was completed?

Experts recommend that a revisedcalculation. When verified, authorized persons may decide that the company delivers tax late. In addition, for the wrong dates, a fine of 500 r. as for unreliable information. They can find any errors and inaccuracies in the document. This provision is explained in the letter of the Federal Tax Service of August 9, 2016. Correcting inaccuracies follows, therefore, even if the office audit is completed, and the inspectors have not reported the revealed shortcomings. Errors can be detected by field inspection. In this case, the organization will be held accountable. It is safer when an error is found immediately pass the specified f. 6-NDFL. This will avoid penalties.